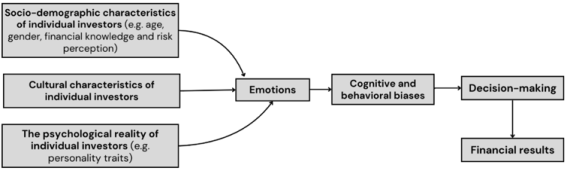

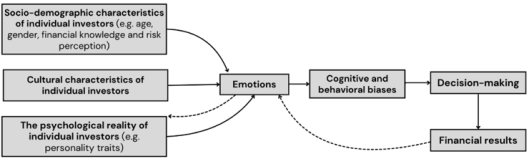

This article describes the set-up of an experimental protocol to take into account the effects of emotional adaptation following stock market decision-making. Basically, the qualitative models used to analyze the behavior of small investors in experimental finance consider three areas of analysis (a socio-demographic analysis, a socio-cultural analysis and an analysis of the psychological reality of individuals). These different areas would then influence the emotions felt, which would stimulate the development of behavioral and cognitive biases. Finally, the latter would ultimately be responsible for influencing decision-making processes. Firstly, our protocol is based on this traditional view of the different factors influencing individual investors' decision-making. Secondly, we suggest a retrospective approach as we believe that the confrontation between expectations and the results generated by decision-making have a feedback effect on the emotional patterns developed by individual investors, and on their psychological reality. Indeed, the increasing number of different emotions tends to "plunge" them into an “emotional bath” in which they can no longer regulate their emotions. This could result in abandonment versus euphoria. According to some authors, “emotional dysregulation” is the result of excessive emotional involvement. Since the stock market is an uncertain environment, where decisions must be made quickly and risks are high, emotional regulation strategies become difficult to apply. Finally, this experimental protocol, supported by qualitative methodological techniques implemented sequentially, makes it possible to analyze emotions as the experiment progresses. We believe this approach offers real added value on two levels. Firstly, even though behavioral finance questions the foundations of traditional finance (and the assumption of rationality), it most often uses quantitative measurement tools. For this purpose, the literature clearly highlights the under-representation of qualitative methodologies in this field. Secondly, the few studies supported by qualitative approaches aim at identifying cause-and-effect links between elements which, in some cases, are difficult to measure and cannot be approached in a linear process. This protocol provides a precise understanding of how emotional patterns and their changes over time might affect the decision-making processes of individual investors.

| Published in | Psychology and Behavioral Sciences (Volume 14, Issue 1) |

| DOI | 10.11648/j.pbs.20251401.12 |

| Page(s) | 7-18 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2025. Published by Science Publishing Group |

Experimental Finance, Qualitative Research, Individual Investors, Emotional Dysregulation, Experimental Design, Decision Making Process, Emotions

Analysis of individual investor decision-making | What ? | When ? | How ? |

|---|---|---|---|

Linear vision | Influence of sociodemographic, cultural and psychological characteristics on the decision-making of individual investors | At the beginning of the experimentation | 1) Questionnaire on age, gender, cultural factors and risk perception 2) Questionnaire on personality traits |

The role of emotions in decision-making | At the end of the experimentation | 1) Questionnaire on emotions 2) Lexico-discursive analysis 3) Semi-structured interviews 4) Focus group(s) | |

Development of cognitive and behavioral biases | At the end of the experimentation | 1) Reading the trading journals 2) Bias questionnaires (items to be assessed on a Likert scale) 3) Semi-structured interviews 4) Focus group(s) | |

Sequential vision | Emotional state | After each phase of the European markets | Questionnaire on emotions |

Expectations of individual investors | After each phase of the European markets | Questionnaire on expectations (Appendix 1) | |

Analysis of orders placed | After each phase of the European markets | Reading the trading journals | |

Retrospective vision | Retroactive effects of past decisions on future strategies | Continuous data collection | Analysis of trading journals based on previous results |

Changes in expectations and adjusting investment strategies | Continuous data collection | Questionnaire on expectations and analysis of trading journals | |

Influence of financial results on emotional state | Continuous data collection | Reading of trading journals and questionnaires on expectations and emotions | |

Changes in personality traits | Continuous data collection | Comparison of initial and final psychological traits |

EEG | Electroencephalogram |

| [1] | Quang, L. T., Linh, N. D., Van Nguyen, D., & Khoa, D. D. (2023). Behavioral factors influencing individual investors' decision making in Vietnam market. Journal of Eastern European and Central Asian Research (JEECAR), 10(2), 264-280. |

| [2] | Madaan, G., & Singh, S. (2020). A systematic review of investment influences of individual investors. TEST: Engineering & Management, 83, 15324-15341. |

| [3] | Wang, Mei & Keller, Carmen & Siegrist, Michael. (2011). The Less You Know, the More You Are Afraid of—A Survey on Risk Perceptions of Investment Products. Journal of Behavioral Finance. 12. 9-19. |

| [4] | Mouna, A., & Anis, J. (2015). A study on small investors’ sentiment, financial literacy and stock returns: evidence for emerging market. International Journal of Accounting and Economics Studies, 3(1), 10-19. |

| [5] | Konteos, G., Konstantinidis, A., & Spinthiropoulos, K. (2018). Representativeness and Investment Decision Making. Journal of Business and Management, 20(2), 5-10. |

| [6] | Chenini, H., & Jarboui, A. (2024). The specific factors of heterogeneity characterizing investors' beliefs. Journal of Economics, Finance and Administrative Science, 29(57), 77-97. |

| [7] | Boyle, G., Hagan, A., O'Connor, R. S., & Whitwell, N. (2004). Emotion, fear and superstition in the New Zealand stockmarket. New Zealand Economic Papers, 38(1), 65-85. |

| [8] | Lovric, M., Kaymak, U. & Spronk, J. (2008). A Conceptual Model of Investor Behavior. ERIM Report Series Reference, ERS-2008-030-F&A, Available at SSRN: |

| [9] | Gabbi, G., & Zanotti, G. (2019). Sex & the City. Are financial decisions driven by emotions? Journal of Behavioral and Experimental finance, 21, 50-57. |

| [10] | Duxbury, D., Gärling, T., Gamble, A., & Klass, V. (2020). How emotions influence behavior in financial markets: a conceptual analysis and emotion-based account of buy-sell preferences. The European Journal of Finance, 26(14), 1417-1438. |

| [11] | Bubić, A., & Erceg, N. (2018). The role of decision making styles in explaining happiness. Journal of Happiness Studies, 19, 213-229. |

| [12] | Iram, T., Bilal, A. R., & Dost, K. (2020). Behavioral Factors Affecting the Investment Decision of an Individual: A Systematic Review. Journal of Xidian University, 14(8), 774-804. |

| [13] | Kumalasari A., Karremans J., Dijksterhuis A., (2022). Do people choose happiness? Anticipated happiness affects both intuitive and deliberative decision-making, Current Psychology, 41, 6500–6510. |

| [14] | Floyd, E., & List, J. A. (2016). Using field experiments in accounting and finance. Journal of Accounting Research, 54(2), 437-475. |

| [15] | Serra, D. (2017). Behavioral Economics. Economica. |

| [16] | Finet, A., Kristoforidis, K., & Viseur, R. (2021). The emergence of behavioral biases in trading situations: an exploratory study. Recherches en Sciences de Gestion, (5), 147-182. |

| [17] | Finet, A., Viseur, R., & Kristoforidis, K. (2022). Decision-making tools in trading situations: an exploratory study. Revue du Financier, 44(248). |

| [18] | Finet, A., Viseur, R., & Kristoforidis, K. (2022). The role of gender in trading activities: An exploratory study. La Revue des Sciences de Gestion, (1), 43-51. |

| [19] | Finet, A., Laznicka, J., & Palumbo, H. (2024). From which planet do they come from? Biases in trading strategies: Does the gender matter? International Journal of Business and Management. 12(12). |

| [20] | Lerner, J. S., Li, Y., Valdesolo, P., & Kassam, K. S. (2015). Emotion and decision making. Annual review of psychology, 66(1), 799-823. |

| [21] | Aren, S., & Aydemir, S. D. (2015). The factors influencing given investment choices of individuals. Procedia-Social and Behavioral Sciences, 210, 126-135. |

| [22] | Kiymaz, H., Öztürkkal, B., & Akkemik, K. A. (2016). Behavioral biases of finance professionals: Turkish evidence.Journal of Behavioral and Experimental Finance, 12, 101-111. |

| [23] | Cueva, C., Iturbe-Ormaetxe, I., Ponti, G., & Tomás, J. (2019). Boys will still be boys: Gender differences in trading activity are not due to differences in (over) confidence. Journal of Economic Behavior & Organization, 160, 100-120. |

| [24] | Faradynawati, I. A. A. (2023). Understanding individual investors’ preferences and knowledge of sustainable investments (Doctoral dissertation, Kungliga Tekniska högskolan). |

| [25] | Sulaiman, E. K. (2012). An empirical analysis of financial risk tolerance and demographic features of individual investors. Procedia Economics and Finance, 2, 109-115. |

| [26] | Bikas, E., Jurevičienė, D., Dubinskas, P., & Novickytė, L. (2013). Behavioural finance: The emergence and development trends. Procedia-social and behavioral sciences, 82, 870-876. |

| [27] | Marinelli, N., Mazzoli, C., & Palmucci, F. (2017). How does gender really affect investment behavior? Economics Letters, 151, 58-61. |

| [28] | Sakthivelu, S., & Karthikeyan, K. (2024). Investors Decision making Behaviour in Insurance Investment Preference. ComFin Research, 12(4), 34-38. |

| [29] | De Bondt, W., Zurstrassen, P., & Arzeni, A. (2001). A psychological portrait of the individual investor in Europe. Revue d'Économie Financière, 131-143. |

| [30] | Ricciardi, V. (2008). The Psychology Of Risk: The Behavioral Finance Perspective. Handbook Of Finance: Volume 2: Investment Management And Financial Management, Frank J. Fabozzi, Ed. Available at SSRN 1155822, 85-111. |

| [31] | Nelson, J. A. (2015). Are women really more risk‐averse than men? A re-analysis of the literature using expanded methods. Journal of economic surveys, 29(3), 566-585. |

| [32] | Lemaster, P., & Strough, J. (2014). Beyond Mars and Venus: Understanding gender differences in financial risk tolerance. Journal of Economic Psychology, 42, 148-160. |

| [33] | Conlin, A., Kyröläinen, P., Kaakinen, M., Järvelin, M. R., Perttunen, J., & Svento, R. (2015). Personality traits and stock market participation. Journal of Empirical Finance, 33, 34-50. |

| [34] | Grassi, G., Pallanti, S., Righi, L., Figee, M., Mantione, M., Denys, D., Piccagliani, D. & Rossi, A., Stratta, P. (2015). Think twice: Impulsivity and decision making in obsessive–compulsive disorder. Journal of Behavioral Addictions. 4. 263-272. |

| [35] | Raheja, S., & Dhiman, B. (2017). Influence of personality traits and behavioral biases on investment decision of investors. Asian Journal of Management, 8(3), 819-826. |

| [36] | Sachdeva, M. and Lehal, R. (2023). The influence of personality traits on investment decision-making: a moderated mediation approach. International Journal of Bank Marketing, 41(4), 810-834. |

| [37] | Lo, A. W., Repin, D. V., & Steenbarger, B. N. (2005). Fear and greed in financial markets: A clinical study of day-traders. American Economic Review, 95(2), 352-359. |

| [38] | Herman, A. M., Critchley, H. D., & Duka, T. (2018). The role of emotions and physiological arousal in modulating impulsive behaviour. Biological psychology, 133, 30-43. |

| [39] | Gambetti, E., & Giusberti, F. (2012). The effect of anger and anxiety traits on investment decisions. Journal of Economic Psychology, 33(6), 1059-1069. |

| [40] | Matsumoto, D., & Wilson, M. (2023). Effects of multiple discrete emotions on risk-taking propensity. Current Psychology, 42(18), 15763-15772. |

| [41] | Chhapra, I. U., Kashif, M., Rehan, R., & Bai, A. (2018). An empirical investigation of investor’s behavioral biases on financial decision making. Asian Journal of Empirical Research, 8(3), 99-109. |

| [42] | Al-Tarawneh, H. A. (2012). The main factors beyond decision making. Journal of Management Research, 4(1), 1-23. |

| [43] | Padmavathy, M. (2024). Behavioral Finance and Stock Market Anomalies: Exploring Psychological Factors Influencing Investment Decisions. Shanlax International Journal of Management, 11(S1), 191-97. |

| [44] | Shukla, A., Dadhich, M., & Dipesh Vaya, A. G. (2024). Impact of Behavioral Biases on Investors' Stock Trading Decisions: A Comparehensive Quantitative Analysis. Indian Journal of Science and Technology, 17(8), 670-678. |

| [45] | Utari, D., Wendy, W., Azazi, A., Giriati, G., & Irdhayanti, E. (2024). The influence of psychological factors on investment decision making. Journal of Management Science (JMAS), 7(1), 299-309. |

| [46] | Xia, Y., & Madni, G. R. (2024). Unleashing the behavioral factors affecting the decision making of Chinese investors in stock markets. PloS One, 19(2), e0298797. |

| [47] | Costa Jr, P. T., & McCrae, R. R. (2000). Neo Personality Inventory. American Psychological Association. |

| [48] | Cloninger, C. R., Bayon, C., & Svrakic, D. M. (1998). Measurement of temperament and character in mood disorders: a model of fundamental states as personality types. Journal of Affective Disorders, 51(1), 21-32. |

| [49] | Harmon-Jones, C., Bastian, B., & Harmon-Jones, E. (2016). The discrete emotions questionnaire: A new tool for measuring state self-reported emotions. PloS One, 11(8). |

| [50] | Mayer, J. D., & Gaschke, Y. N. (1988). The experience and meta-experience of mood. Journal of Personality and Social Psychology, 55, 102-111. |

| [51] | Mehrabian, A., & Russell, J. A. (1974). An approach to environmental psychology. Cambridge, MA: MIT Press. |

| [52] | Waddington, K. (2012). Using qualitative diary research to understand emotion at work. A Day in the Life of a Happy Worker, 132-149, Psychology Press. |

| [53] | Scott, S. (2022). ‘I enjoy having someone to rant to, I feel like someone is listening to me’: Exploring emotion in the use of qualitative, longitudinal diary-based methods. International Journal of Qualitative Methods, 21. |

| [54] | Touré, E. H. (2010). Epistemological reflection on the use of focus groups: Scientific foundations and problems of scientific validity. Recherches Qualitatives, 29(1), 5-27. |

| [55] | Pin, C. (2023). The Semi-Structured Interview. LIEPP Methods Brief from LIEPP. |

| [56] | Rabiee, F. (2004). Focus-group interview and data analysis. Proceedings of the nutrition society, 63(4), 655-660. |

| [57] | Akyıldız, S. T., & Ahmed, K. H. (2021). An overview of qualitative research and focus group discussion. International Journal of Academic Research in Education, 7(1), 1-15. |

| [58] | Porter, D. P., & Smith, V. L. (2003). Stock market bubbles in the laboratory. The Journal of Behavioral Finance, 4(1), 7-20. |

| [59] | Fréchette, G. R. (2011). Laboratory experiments: Professionals versus students. Available at SSRN 1939219. |

| [60] | Rossignol, M., Anselme, C., Vermeulen, N., Philippot, P., & Campanella, S. (2007). Categorical perception of anger and disgust facial expression is affected by non-clinical social anxiety: an ERP study. Brain research, 1132, 166-176. |

| [61] | She, S., Eimontaite, I., Zhang, D., & Sun, Y. (2017). Fear, anger, and risk preference reversals: An experimental study on a Chinese sample. Frontiers in Psychology, 8, 1371. |

| [62] | Bell, D. E. (1982). Regret in decision making under uncertainty. Operations research, 30(5), 961-981. |

| [63] | Ratner, R. K., & Herbst, K. C. (2005). When good decisions have bad outcomes: The impact of affect on switching behavior. Organizational Behavior and Human Decision Processes, 96(1), 23-37. |

| [64] | Domeignoz, C., & Morin, E. (2016). Emotions Have their Reasons: We Should Listen to Them. Entreprendre & Innover, (2), 7-15. |

| [65] | Gross, J. J. (1998). The emerging field of emotion regulation: An integrative review. Review of general psychology, 2(3), 271-299. |

| [66] | Larsen, R. J. (2000). Toward a science of mood regulation. Psychological inquiry, 11(3), 129-141. |

| [67] | Quoidbach, J., Berry, E. V., Hansenne, M., & Mikolajczak, M. (2010). Positive emotion regulation and well-being: Comparing the impact of eight savoring and dampening strategies. Personality and individual differences, 49(5), 368-373. |

| [68] | Tamir, M., John, O. P., Srivastava, S., & Gross, J. J. (2007). Implicit theories of emotion: affective and social outcomes across a major life transition. Journal of personality and social psychology, 92(4), 731. |

| [69] | De Castella, K., Platow, M. J., Tamir, M., & Gross, J. J. (2018). Beliefs about emotion: Implications for avoidance-based emotion regulation and psychological health. Cognition and Emotion, 32(4), 773-795. |

| [70] | Gross, J. J. (2014). Emotion regulation: Conceptual and empirical foundations. Handbook of emotion regulation, 2, 3-20. |

| [71] | Troy, A. S., Shallcross, A. J., & Mauss, I. B. (2013). A person-by-situation approach to emotion regulation: Cognitive reappraisal can either help or hurt, depending on the context. Psychological Science, 24, 2505–2514. |

| [72] | Gross, J. J., & Levenson, R. W. (1993). Emotional suppression: Physiology, self-report, and expressive behavior. Journal of Personality and Social Psychology, 64, 970–986. |

| [73] | Gross, J. J., & John, O. P. (2003). Individual differences in two emotion regulation processes: Implications for affect, relationships, and well-being. Journal of Personality and Social Psychology, 85, 348–362. |

| [74] | Chambers, R., Gullone, E., & Allen, N. B. (2009). Mindful emotion regulation: An integrative review. Clinical psychology review, 29(6), 560-572. |

| [75] | Sheppes, G., & Meiran, N. (2007). Better late than never? On the dynamics of online regulation of sadness using distraction and cognitive reappraisal. Personality and Social Psychology Bulletin, 33(11), 1518-1532. |

| [76] | Seban, O. (2007). Day Trading and Swing Trading Techniques and Strategies: 2nd revised and expanded edition. Maxima Laurent du Mesnil Éditeur. |

| [77] | Kabbaj, T. (2011). Famous Traders Psychology. Editions Eyrolles. |

| [78] | Cushing, D., & Madhavan, A. (2000). Stock returns and trading at the close. Journal of Financial Markets, 3(1), 45-67. |

| [79] | Bacidore, J., Polidore, B., Xu, W., & Yang, C. (2013). Trading around the close. The Journal of Trading, 8(1), 48-57. |

| [80] | Asutay, E., & Västfjäll, D. (2024). Affective integration in experience, judgment, and decision-making. Communications Psychology, 2(1), 126. |

| [81] | Wu, G., Zhang, J., & Gonzalez, R. (2004). Decision under risk. Blackwell handbook of judgment and decision making, 399-423. |

| [82] | Lee, B., Rosenthal, L., Veld, C., & Veld-Merkoulova, Y. (2015). Stock market expectations and risk aversion of individual investors. International Review of Financial Analysis, 40, 122-131. |

APA Style

Finet, A., Laznicka, J. (2025). Addressing Emotional Dysregulation in Experimental Design. Psychology and Behavioral Sciences, 14(1), 7-18. https://doi.org/10.11648/j.pbs.20251401.12

ACS Style

Finet, A.; Laznicka, J. Addressing Emotional Dysregulation in Experimental Design. Psychol. Behav. Sci. 2025, 14(1), 7-18. doi: 10.11648/j.pbs.20251401.12

AMA Style

Finet A, Laznicka J. Addressing Emotional Dysregulation in Experimental Design. Psychol Behav Sci. 2025;14(1):7-18. doi: 10.11648/j.pbs.20251401.12

@article{10.11648/j.pbs.20251401.12,

author = {Alain Finet and Julie Laznicka},

title = {Addressing Emotional Dysregulation in Experimental Design

},

journal = {Psychology and Behavioral Sciences},

volume = {14},

number = {1},

pages = {7-18},

doi = {10.11648/j.pbs.20251401.12},

url = {https://doi.org/10.11648/j.pbs.20251401.12},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.pbs.20251401.12},

abstract = {This article describes the set-up of an experimental protocol to take into account the effects of emotional adaptation following stock market decision-making. Basically, the qualitative models used to analyze the behavior of small investors in experimental finance consider three areas of analysis (a socio-demographic analysis, a socio-cultural analysis and an analysis of the psychological reality of individuals). These different areas would then influence the emotions felt, which would stimulate the development of behavioral and cognitive biases. Finally, the latter would ultimately be responsible for influencing decision-making processes. Firstly, our protocol is based on this traditional view of the different factors influencing individual investors' decision-making. Secondly, we suggest a retrospective approach as we believe that the confrontation between expectations and the results generated by decision-making have a feedback effect on the emotional patterns developed by individual investors, and on their psychological reality. Indeed, the increasing number of different emotions tends to "plunge" them into an “emotional bath” in which they can no longer regulate their emotions. This could result in abandonment versus euphoria. According to some authors, “emotional dysregulation” is the result of excessive emotional involvement. Since the stock market is an uncertain environment, where decisions must be made quickly and risks are high, emotional regulation strategies become difficult to apply. Finally, this experimental protocol, supported by qualitative methodological techniques implemented sequentially, makes it possible to analyze emotions as the experiment progresses. We believe this approach offers real added value on two levels. Firstly, even though behavioral finance questions the foundations of traditional finance (and the assumption of rationality), it most often uses quantitative measurement tools. For this purpose, the literature clearly highlights the under-representation of qualitative methodologies in this field. Secondly, the few studies supported by qualitative approaches aim at identifying cause-and-effect links between elements which, in some cases, are difficult to measure and cannot be approached in a linear process. This protocol provides a precise understanding of how emotional patterns and their changes over time might affect the decision-making processes of individual investors.

},

year = {2025}

}

TY - JOUR T1 - Addressing Emotional Dysregulation in Experimental Design AU - Alain Finet AU - Julie Laznicka Y1 - 2025/02/20 PY - 2025 N1 - https://doi.org/10.11648/j.pbs.20251401.12 DO - 10.11648/j.pbs.20251401.12 T2 - Psychology and Behavioral Sciences JF - Psychology and Behavioral Sciences JO - Psychology and Behavioral Sciences SP - 7 EP - 18 PB - Science Publishing Group SN - 2328-7845 UR - https://doi.org/10.11648/j.pbs.20251401.12 AB - This article describes the set-up of an experimental protocol to take into account the effects of emotional adaptation following stock market decision-making. Basically, the qualitative models used to analyze the behavior of small investors in experimental finance consider three areas of analysis (a socio-demographic analysis, a socio-cultural analysis and an analysis of the psychological reality of individuals). These different areas would then influence the emotions felt, which would stimulate the development of behavioral and cognitive biases. Finally, the latter would ultimately be responsible for influencing decision-making processes. Firstly, our protocol is based on this traditional view of the different factors influencing individual investors' decision-making. Secondly, we suggest a retrospective approach as we believe that the confrontation between expectations and the results generated by decision-making have a feedback effect on the emotional patterns developed by individual investors, and on their psychological reality. Indeed, the increasing number of different emotions tends to "plunge" them into an “emotional bath” in which they can no longer regulate their emotions. This could result in abandonment versus euphoria. According to some authors, “emotional dysregulation” is the result of excessive emotional involvement. Since the stock market is an uncertain environment, where decisions must be made quickly and risks are high, emotional regulation strategies become difficult to apply. Finally, this experimental protocol, supported by qualitative methodological techniques implemented sequentially, makes it possible to analyze emotions as the experiment progresses. We believe this approach offers real added value on two levels. Firstly, even though behavioral finance questions the foundations of traditional finance (and the assumption of rationality), it most often uses quantitative measurement tools. For this purpose, the literature clearly highlights the under-representation of qualitative methodologies in this field. Secondly, the few studies supported by qualitative approaches aim at identifying cause-and-effect links between elements which, in some cases, are difficult to measure and cannot be approached in a linear process. This protocol provides a precise understanding of how emotional patterns and their changes over time might affect the decision-making processes of individual investors. VL - 14 IS - 1 ER -

Health Institute, Financial Management Department, University of Mons, Mons, Belgium

Research Fields: Alain Finet: Corporate Governance, Market Efficiency, Event Studies, Behavioral Finance, Qualitative Research Methodology, Emotions, Cognitive Bias

Health Institute, Financial Management Department, University of Mons, Mons, Belgium

Research Fields: Julie Laznicka: Qualitative Research Methodology, Emotions, Cognitive Bias